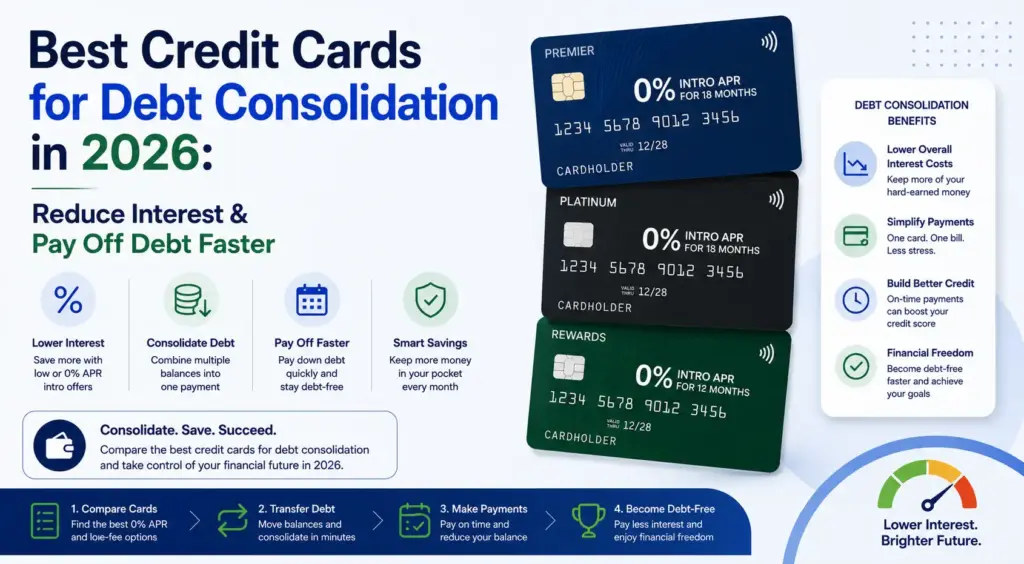

Managing high-interest credit card debt has become a major financial challenge for many consumers. With changing interest rates, increasing living costs, and expensive borrowing options, finding smarter ways to reduce debt is more important than ever.

In 2026, a debt consolidation credit card with a long 0% introductory APR balance transfer offer can help borrowers lower interest costs, simplify payments, and accelerate their journey toward financial freedom.

This guide covers the best credit cards for debt consolidation, how they work, potential savings, and strategies to pay off debt faster.

What Is a Debt Consolidation Credit Card?

A debt consolidation credit card is designed to combine multiple high-interest debts into one account, usually with a low or 0% promotional APR.

Instead of paying high monthly interest charges, borrowers can move existing balances to a new card and focus payments on reducing the principal balance.

How Debt Consolidation Works:

- Apply for a credit card with a balance transfer offer

- Move existing credit card balances to the new account

- Take advantage of the introductory APR period

- Pay down the debt before the promotional period ends

The goal is simple: reduce interest expenses and create a structured repayment plan.

Benefits of Using a Debt Consolidation Credit Card

A well-selected consolidation card can provide several financial advantages.

Lower Interest Costs

A 0% APR balance transfer can significantly reduce interest payments compared with traditional high-interest credit cards.

Simplified Debt Management

Instead of tracking multiple accounts, borrowers can manage one monthly payment.

Faster Debt Repayment

More of each payment goes toward the actual balance rather than interest charges.

Potential Credit Score Improvement

Lower credit utilization and consistent payments may help improve credit health over time.

No Collateral Required

Unlike secured loans, most credit card consolidation options do not require assets as security.

What to Look for in a Debt Consolidation Card in 2026

Not every balance transfer card offers the same value. Compare these important factors:

1. Introductory APR Period

The longer the 0% APR period, the more time you have to eliminate debt without interest.

Look for offers ranging from 18–24 months or longer.

2. Balance Transfer Fee

Most cards charge a transfer fee, commonly between 3% and 5%.

Always calculate whether the interest savings are greater than the transfer cost.

3. Regular APR After Promotion

If you do not finish repayment before the promotional period ends, the remaining balance may receive a higher standard APR.

4. Credit Limit

A higher credit limit allows you to consolidate more debt into one account.

5. Fees and Terms

Review:

- Annual fees

- Late payment penalties

- Foreign transaction fees

- Purchase APR

- Eligibility requirements

Top 7 Best Credit Cards for Debt Consolidation in 2026

1. Reflect® 0% APR Balance Transfer Card — Best Overall

The Reflect® balance transfer option is designed for borrowers who need maximum time to eliminate debt.

Features:

- Long introductory APR period

- No annual fee

- Flexible repayment timeline

- Helpful for large balances

Best for: Consumers who want maximum interest savings.

2. Citi Simplicity® Card — Best for Flexible Repayment

Citi provides credit products known for simple account management and consumer-friendly features.

Features:

- Introductory APR offers

- No penalty APR features

- Easy online banking management

- Flexible payment options

Best for: Borrowers who prefer simple debt management.

3. Discover it® Balance Transfer — Best for Rewards

Discover Financial Services combines balance transfer options with cashback opportunities.

Features:

- Promotional APR offers

- Cashback rewards

- No annual fee options

- Digital financial tools

Best for: Users wanting rewards while reducing debt.

4. Chase Slate Edge℠ — Best for Credit Improvement

JPMorgan Chase offers credit card solutions with financial management tools.

Features:

- Balance transfer promotions

- Credit monitoring tools

- Mobile banking access

- Trusted banking services

Best for: Borrowers improving credit habits.

5. BankAmericard® — Best for Predictable Terms

Bank of America offers balance transfer options designed for consumers seeking straightforward repayment.

Features:

- Intro APR periods

- Online account management

- Competitive terms

- Established financial services

Best for: Consumers who want simplicity.

6. Wells Fargo Balance Transfer Cards — Best for Large Balances

Wells Fargo offers credit card products with balance transfer features.

Features:

- High credit limit potential

- Digital banking tools

- Customer support services

- Flexible repayment options

Best for: Larger debt consolidation needs.

7. Credit Union Balance Transfer Cards — Best Low-Fee Alternative

Credit unions often provide competitive balance transfer offers for eligible members.

Features:

- Lower fees

- Member-focused lending

- Flexible approval options

- Competitive interest rates

Best for: Borrowers looking for affordable alternatives.

How Much Money Can Debt Consolidation Save?

Example:

Current debt: $7,500

Credit card APR: 22%

Monthly payment: $250

Without consolidation:

- Higher interest charges

- Longer repayment period

- More money spent overall

With a 0% APR balance transfer:

- Transfer fee: approximately $225 (3%)

- Reduced interest cost

- Faster principal reduction

- Potential savings of thousands of dollars

Actual savings depend on repayment amount, fees, and promotional period.

Step-by-Step Debt Consolidation Strategy

Step 1: Calculate Your Total Debt

List:

- Credit card balances

- Interest rates

- Minimum payments

Step 2: Compare Credit Card Offers

Look for:

- Long 0% APR periods

- Low transfer fees

- Suitable credit limits

Step 3: Transfer Eligible Balances

Complete transfers during the promotional window.

Step 4: Create a Repayment Plan

Divide your total balance by the number of months in the intro period.

Step 5: Avoid New Debt

Stop adding purchases while paying off existing balances.

Step 6: Use Automatic Payments

Autopay helps avoid missed payments and protects promotional benefits.

Common Debt Consolidation Mistakes

Using the New Card for Spending

Adding new purchases can recreate the same debt problem.

Paying Only Minimum Payments

Minimum payments may not eliminate debt before the promotional APR expires.

Ignoring Transfer Fees

Always calculate the full cost before moving balances.

Closing Old Credit Cards Immediately

Closing accounts may impact your credit history and utilization ratio.

Applying for Too Many Cards

Multiple applications may affect your credit profile.

Who Should Use a Debt Consolidation Credit Card?

These cards are ideal for people who:

- Have high-interest credit card debt

- Have good credit scores

- Want to reduce interest payments

- Need a structured repayment plan

- Are committed to avoiding new debt

A personal loan may be a better option for borrowers who need fixed payments and longer repayment terms.

Final Verdict: Best Debt Consolidation Cards in 2026

A debt consolidation credit card can be one of the most effective personal finance tools when used correctly.

The best options combine:

✔ Long 0% APR periods

✔ Low balance transfer fees

✔ Strong banking security

✔ Flexible repayment options

✔ Clear terms and conditions

With a disciplined repayment strategy, these cards can reduce interest costs, simplify debt management, and help you move closer to financial independence in 2026.