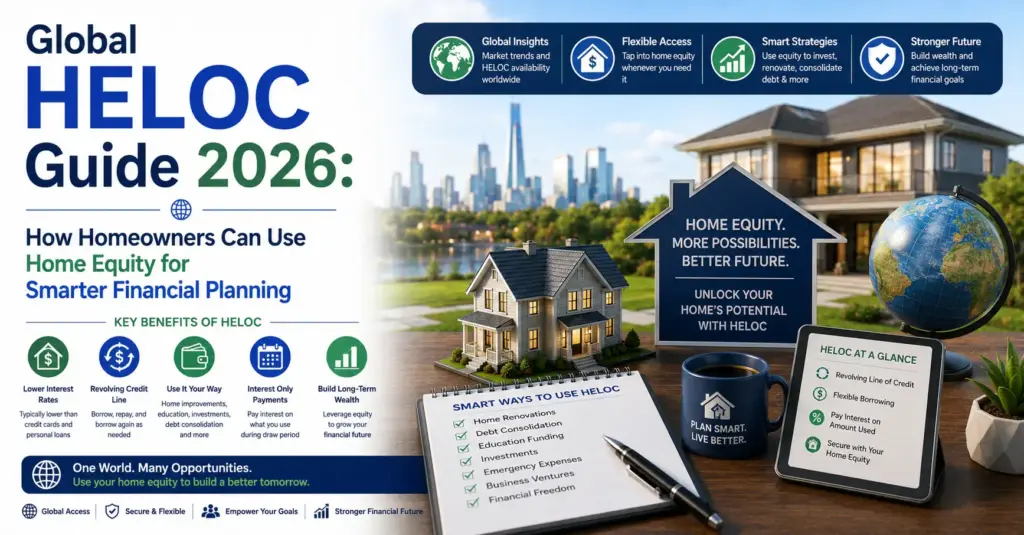

Your home is one of your most valuable financial assets. As property values increase and mortgage balances decrease, homeowners build equity that can be used as a powerful financial resource.

A Home Equity Line of Credit (HELOC) is one of the most flexible ways to access home equity while maintaining control over borrowing.

Unlike traditional loans, a HELOC allows homeowners to borrow, repay, and borrow again — creating a flexible financing solution for:

- Home renovations

- Debt consolidation

- Emergency expenses

- Education costs

- Business opportunities

- Long-term financial planning

This global HELOC guide explains how a home equity line of credit works, qualification requirements, benefits, risks, interest rates, and smart strategies for homeowners in 2026.

What Is a HELOC (Home Equity Line of Credit)?

A HELOC is a revolving secured credit line backed by your home’s equity.

It works similarly to a credit card, but usually offers lower interest rates because the borrowing is secured by property.

With a HELOC, you receive a credit limit based on:

- Home value

- Existing mortgage balance

- Credit profile

- Income

- Debt obligations

You can access funds when needed and only pay interest on the amount borrowed.

How Does a HELOC Work?

A HELOC usually has two main stages.

1. Draw Period

Typically lasting several years, the draw period allows homeowners to:

- Withdraw funds

- Make payments

- Reuse available credit

Some lenders allow interest-only payments during this stage.

2. Repayment Period

After the draw period ends, homeowners repay the remaining balance.

Payments may include:

- Principal

- Interest

- Applicable fees

Monthly payments may increase during repayment.

Global Availability of HELOC Products

HELOC-style financing is available in many major housing markets.

United States

One of the largest HELOC markets globally, with many banks and mortgage lenders offering home equity financing.

Canada

Home equity credit products are widely used for renovations and financial management.

United Kingdom

Similar products may appear as:

- Secured homeowner loans

- Revolving credit facilities

- Equity-based lending

Australia and New Zealand

Property-backed lending products are available through major financial institutions.

Asia and Emerging Markets

Countries such as Singapore, Hong Kong, UAE, and India offer similar options under different names, including:

- Property-backed loans

- Top-up loans

- Secured credit lines

HELOC vs Home Equity Loan: Key Difference

Homeowners often compare these two products.

HELOC

Best for:

- Flexible borrowing

- Ongoing expenses

- Uncertain costs

Features:

- Revolving credit

- Variable interest rate

- Borrow only what you need

Home Equity Loan

Best for:

- Large one-time expenses

- Predictable repayment

Features:

- Lump sum payment

- Fixed interest rate

- Fixed monthly payments

How Much Equity Do You Need for a HELOC?

Requirements vary by lender and country.

Many lenders require homeowners to maintain a certain percentage of equity.

A common calculation uses:

Loan-to-Value Ratio (LTV)

Example:

Home value:

$400,000

Mortgage balance:

$250,000

Available equity:

$150,000

A lender may approve a portion of that equity depending on:

- Credit score

- Income

- Property type

- Lending rules

HELOC Qualification Requirements

Lenders usually review:

Credit Score

A stronger credit score may help you receive:

- Better HELOC rates

- Higher credit limits

- Lower fees

Stable Income

Lenders want confidence that borrowers can manage payments.

Debt-to-Income Ratio (DTI)

A lower DTI improves approval chances.

Home Appraisal

The lender evaluates your property value before approving the credit line.

How HELOC Interest Rates Work

Most HELOCs use variable interest rates linked to market benchmarks.

This means your payments may change over time.

Your rate can depend on:

- Central bank policies

- Market conditions

- Lender pricing

- Credit profile

Some lenders offer:

- Fixed-rate conversion options

- Hybrid HELOC products

- Rate protection features

Benefits of a HELOC

Flexible Access to Money

Borrow funds only when needed.

This is useful for unpredictable expenses.

Lower Interest Than Many Alternatives

HELOCs may have lower rates compared with:

- Credit cards

- Personal loans

- Unsecured debt

Reusable Credit

As you repay the balance, available credit may become usable again.

Home Improvement Financing

HELOCs are commonly used for projects that may increase property value.

Examples:

- Remodeling

- Repairs

- Energy upgrades

- Property improvements

Debt Consolidation

Many homeowners use HELOC financing to replace high-interest debt with lower-cost secured borrowing.

Risks and Disadvantages of HELOCs

A HELOC can be useful, but homeowners should understand the risks.

Variable Interest Rates

Payments may increase if interest rates rise.

Your Home Is Collateral

Failure to repay may put your property at risk.

Overborrowing

Easy access to credit can encourage unnecessary spending.

Changing Property Values

A decline in home value can reduce available equity.

Smart Ways to Use a HELOC

1. Home Renovations

One of the strongest uses of a HELOC is improving your property.

Well-planned upgrades may increase:

- Home value

- Comfort

- Market appeal

2. Debt Consolidation

A HELOC may help reduce expensive debt costs.

Common targets:

- Credit card balances

- High-interest loans

- Multiple monthly payments

3. Emergency Financial Backup

A HELOC can provide access to funds for:

- Major repairs

- Medical expenses

- Unexpected costs

4. Education Funding

Some families use home equity financing for:

- Tuition

- Professional education

- Overseas study expenses

5. Business Funding

Entrepreneurs may use HELOC funds for:

- Startup costs

- Equipment purchases

- Business cash flow

When Should You Avoid a HELOC?

A HELOC may not be suitable if:

- Income is unstable

- You cannot manage variable payments

- You plan unnecessary spending

- You are using it for risky investments

- You may move soon

HELOC Application Process

Typical steps include:

Step 1: Check Your Credit

Review your credit profile before applying.

Step 2: Estimate Home Equity

Determine your approximate property value.

Step 3: Compare HELOC Lenders

Compare:

- Interest rates

- Fees

- Credit limits

- Repayment terms

Step 4: Submit Documents

Common requirements:

- Income proof

- Mortgage information

- Property documents

Step 5: Property Evaluation

The lender completes appraisal and underwriting.

HELOC vs Refinance: Which Is Better?

Choose a HELOC if you need:

✓ Flexible access to funds

✓ Smaller or repeated borrowing

✓ Home improvement financing

Choose refinancing if you need:

✓ Lower mortgage payments

✓ A new mortgage rate

✓ A large lump sum through cash-out refinance

Future of HELOC Lending in 2026

The home equity market continues evolving with:

- Digital loan applications

- Faster approvals

- AI-powered underwriting

- Automated property valuation

- More competitive lenders

Technology is making home equity financing easier and faster for homeowners.

Final Thoughts: Using Home Equity Wisely

A HELOC can be a powerful financial planning tool when used responsibly.

It provides homeowners with:

- Flexible borrowing

- Affordable secured credit

- Access to property wealth

- Financial flexibility

However, because your home secures the loan, careful planning is essential.

By comparing HELOC rates, reviewing lenders, and borrowing strategically, homeowners can maximize their home equity while protecting long-term financial security.

Understanding Mortgage Amortization 2026: How Your Home Loan Really Works

A mortgage is one of the largest financial commitments most people make, yet many homeowners do not fully understand how their monthly payments are calculated.

Understanding mortgage amortization can help you make smarter decisions when buying a home, refinancing, choosing a loan term, or planning long-term financial goals.

A clear understanding of amortization helps homeowners:

- Reduce total interest costs

- Pay off their mortgage faster

- Choose better loan options

- Compare mortgage offers

- Improve financial planning

This guide explains how mortgage amortization works, how payments are structured, and strategies to save money over the life of your home loan.

What Is Mortgage Amortization?

Mortgage amortization is the process of gradually paying off a home loan through scheduled monthly payments.

Each mortgage payment is divided into two parts:

Principal

The principal is the original amount borrowed from the lender.

Interest

Interest is the cost of borrowing money.

At the beginning of the mortgage, a larger portion of your payment usually goes toward interest because the outstanding balance is higher.

As the loan balance decreases, more of your payment goes toward reducing the principal.

How Mortgage Amortization Works

A typical amortized mortgage includes:

- Loan amount

- Interest rate

- Loan term

- Monthly payment amount

- Payment schedule

For example, a 30-year mortgage spreads repayment across hundreds of monthly payments.

Each payment reduces the balance until the loan reaches zero.

Global Mortgage Amortization Explained

Mortgage amortization is widely used in housing markets around the world.

Countries including:

- United States

- Canada

- United Kingdom

- Australia

- New Zealand

- Singapore

- European markets

commonly use structured home loan repayment systems.

Although mortgage terms and regulations vary, the basic principle remains the same:

Borrow money → Make scheduled payments → Reduce balance → Own the property fully.

Benefits of an Amortized Mortgage

Predictable Monthly Payments

A fixed amortization schedule helps homeowners plan expenses.

You can estimate:

- Monthly mortgage payments

- Total repayment cost

- Interest expenses

Clear Debt Repayment Timeline

Unlike revolving credit, amortized loans have a defined end date.

You know when your mortgage will be fully paid.

Builds Home Equity

Every principal payment increases your ownership stake in the property.

Over time, your equity grows through:

- Mortgage repayment

- Property appreciation

Potential Interest Savings

Strategic payments can reduce the amount of interest paid over the loan term.

Understanding an Amortization Schedule

An amortization schedule is a detailed table showing every mortgage payment.

It includes:

- Payment number

- Monthly payment

- Interest portion

- Principal portion

- Remaining loan balance

A mortgage amortization calculator can help borrowers visualize how payments change over time.

Why Early Mortgage Payments Are Mostly Interest

Many homeowners are surprised that early payments reduce the balance slowly.

This happens because interest is calculated based on the remaining loan balance.

At the beginning:

- Loan balance is high

- Interest charges are higher

- Principal reduction is smaller

Later:

- Balance decreases

- Interest decreases

- More money goes toward principal

Example of Mortgage Payment Structure

Imagine a homeowner has a mortgage balance of $400,000.

In the early years:

A larger share of the monthly payment may cover interest.

After several years:

The principal portion increases as the balance declines.

This gradual shift is the foundation of mortgage amortization.

How to Reduce Mortgage Interest Costs

Homeowners can lower total borrowing costs through smart strategies.

1. Make Extra Principal Payments

Additional payments directly reduce your mortgage balance.

Benefits:

- Lower interest charges

- Faster payoff

- Increased home equity

Even small extra payments can create significant savings over time.

2. Choose Biweekly Payments

Instead of making one monthly payment, some homeowners choose payments every two weeks.

This may result in:

- Extra annual payments

- Faster principal reduction

- Lower total interest

3. Refinance Your Mortgage

When mortgage rates decrease, refinancing may help homeowners secure:

- Lower interest rates

- Reduced monthly payments

- Shorter loan terms

Comparing mortgage refinance rates can help determine if refinancing makes financial sense.

4. Select a Shorter Loan Term

A 15-year mortgage usually costs less in total interest compared with a 30-year mortgage.

However, monthly payments are higher.

Factors That Affect Mortgage Amortization

Your amortization schedule depends on:

Interest Rate

Higher rates increase total interest costs.

Loan Term

Longer loans reduce monthly payments but increase total interest.

Loan Amount

Larger mortgages require more repayment.

Payment Frequency

More frequent payments can accelerate payoff.

Extra Payments

Additional principal payments shorten the repayment timeline.

Fixed vs Adjustable Mortgage Amortization

Fixed-Rate Mortgage

Payments remain predictable.

Benefits:

- Stable budgeting

- Protection from rate increases

- Long-term certainty

Adjustable-Rate Mortgage (ARM)

Interest rates may change over time.

Benefits:

- Lower initial rates

- Potential short-term savings

Risks:

- Payment increases when rates rise

Interest-Only vs Amortized Mortgages

Some markets offer interest-only loans.

With interest-only loans:

- Early payments cover interest

- Principal may remain unchanged

Advantages:

- Lower initial payments

Disadvantages:

- Slower equity growth

- Higher future payments

Traditional amortized mortgages remain popular because they steadily reduce debt.

Mortgage Amortization and Refinancing Strategy

Refinancing can change your amortization schedule.

Homeowners refinance to:

- Reduce interest rates

- Lower monthly payments

- Pay off debt faster

- Access home equity

A refinance decision should consider:

- Closing costs

- New loan term

- Total interest savings

Common Mortgage Amortization Mistakes

Ignoring Total Interest Cost

A low monthly payment does not always mean a cheaper mortgage.

Always compare:

- APR

- Total repayment amount

- Loan duration

Choosing the Longest Loan Without Planning

Longer terms can increase lifetime interest expenses.

Not Reviewing Prepayment Rules

Some mortgages may include restrictions or penalties for early repayment.

Who Benefits Most From Understanding Amortization?

Understanding amortization helps:

- First-time homebuyers

- Real estate investors

- Refinancing homeowners

- Property owners

- Long-term financial planners

Knowledge of repayment structure leads to better borrowing decisions.

Final Thoughts: Master Your Mortgage Repayment

Mortgage amortization is the foundation of how most home loans work.

By understanding:

- Principal payments

- Interest costs

- Loan terms

- Repayment strategies

homeowners can make smarter financial decisions.

Whether you are purchasing a home, refinancing, or planning your financial future, understanding amortization can help you reduce costs, build equity faster, and maximize the value of your home financing strategy.